by Manuel Alvarez-Rivera, Puerto Rico

The Czech Republic will be holding an early general election later this year - nearly a year ahead of schedule - after the center-right coalition government of Prime Minister Mirek Topolánek was brought down last week in a parliamentary no-confidence vote. Topolánek, who submitted his resignation last Thursday but remains as caretaker head of government and leader of the Civic Democratic Party (ODS) - the largest party in the Central European country's bicameral legislature - subsequently reached an agreement with former Prime Minister Jiří Paroubek, the leader of the Czech Social Democratic Party (ČSSD) - the main opposition force - to hold an early poll next October; a specific date remains to be determined.

Prime Minister Topolánek came to office following a closely fought general election in June 2006, which left the Chamber of Deputies - the lower house of the Czech Parliament - evenly split between left- and right-wing parties. However, in early 2007 Topolánek was able to secure a parliamentary majority with the help of two rebel ČSSD deputies, and he went on to survive four no-confidence motions during the course of 2007 and 2008. Nonetheless, his government depended upon a fragile majority, which was finally shattered when four dissident deputies - two from ODS, plus two recently expelled from the Green Party (SZ) - sided with ČSSD and the Communist Party of Bohemia and Moravia (KSČM) to pass by 101-96 a vote of no-confidence.

Coincidentally, the fall of the Czech government came on the same day that Topolánek - who currently holds the European Union's rotating presidency - made headlines around the world when he criticized the economic stimulus program of U.S. President Barack Obama as "the road to hell." While the vote of confidence was triggered by allegations of abuse of state subsidies by a deputy who left ČSSD to support ODS, some opposition deputies voted to bring down Topolánek as a protest against his government's economic policies, which according to them failed to deal effectively with the global financial crisis; although the Czech economy is not in as dire straits as those of other nearby countries (such as Hungary), the Czech Republic is nonetheless forecast to suffer a recession this year.

Opinion polls have ČSSD ahead of ODS; that said, the gap between the two parties appears to be narrowing down. Nonetheless, the Social Democrats are hoping for a repeat of their performance in last October's regional and Senate elections, in which ČSSD captured 23 of 27 Senate mandates up for renewal, depriving ODS of its absolute majority in the upper house of Parliament. Although it has some ex-Communist members, ČSSD is not a post-Communist party; unlike major left-of-center parties in other Eastern European countries, it traces its roots to the Social Democratic Party that was forcibly merged with the Communists in 1948. However, the Czech Social Democrats have to compete on the left with the Communists, who still command a significant following.

The Czech Chamber of Deputies is elected by party-list proportional representation in regional constituencies - Parliamentary Elections in the Czech Republic has a review of the Czech electoral system - and no single party has ever commanded an absolute lower house majority. Moreover, the ongoing presence of a sizable, unreformed Communist Party has greatly complicated the task of forming stable governments in the Czech Republic. While the Social Democrats have called upon Communist support from time to time (as they did for last week's no-confidence vote), neither them nor the parties to their right regard the Communists as suitable coalition partners, largely for historical reasons: save for the short-lived "Prague Spring" of 1968, the Communist Party governed Czechoslovakia - the now-defunct federation of the Czech Republic and Slovakia - in a totalitarian fashion from 1948 to 1989, when the Velvet Revolution put an end to the Communist regime.

As a result, since 1996 the Czech Republic has been ruled either by shaky coalition cabinets, such as those formed from 2002 to 2006 by ČSSD and the four party coalition headed by the Christian and Democratic Union-Czechoslovak People's Party (KDU-ČSL), and from 2007 to the present by ODS, KDU-ČSL and SZ; or by minority governments dependent upon the good will of the opposition, as was the case from 1998 to 2002, when ODS reached an "opposition agreement" with ČSSD under which the Civic Democrats tolerated Milos Zeman's minority Social Democratic government without supporting it.

In fact, Topolánek may have to reach out to the Social Democrats in order to secure Senate passage of the Lisbon Treaty, which would streamline the functioning of the European Union. While Topolánek is in favor of the treaty, many Euroskeptics in ODS remain opposed to it, as is President Vaclav Klaus, the former leader of the Civic Democrats.

At this juncture, it remains unclear what will happen to Prime Minister Topolánek's outgoing government until the election is held. ČSSD leader Paroubek declared that he is willing to tolerate the government until the end of June (when Sweden takes over the EU presidency) if certain conditions are met, but favors the appointment of an interim government of non-party experts after that date. Meanwhile, Topolánek insists on remaining in office, but he and President Klaus - who has the right to appoint the next government - are political enemies, and not surprisingly Klaus is proposing the formation of a new cabinet without further delay. However, Czech governments require majority support in the Chamber of Deputies in order to remain in office, and in light of last week's events it appears rather unlikely that such support would be forthcoming.

Monday, March 30, 2009

Japan - Engine Failure

By Claus Vistesen: Copenhagen

Last time I had Japan under the loop I asked whether there was no end in sight for Japan's economy and as I wind up for another close look, I must say that it is still very difficult to find good news if any at all. However, and for the sake of argument I thought that we might begin with some recent arguments in the context of the global economy which suggest that we may be past the worst of our travails. The first observation comes from the Economist's ever eloquent financial markets pundit, Buttonwood, who recently made the neat point that while we are still stuck in the mire, the second derivative might be turning positive. This suggests that while indicators are still on the decline they are now declining less rapidly. In Tokyo, Cassandra voices a similar sentiment as she takes stock of the number presented earlier last week by the Asian Development Bank that as much as USD 50 trillion, so far, has vanished into thin air during this crisis. Hovering between the "half full, half empty" metaphor Cass notes;

For the moment, I'll take the middle ground and venture that having shed an awful lot of aggregate value (an entire year of global GDP according to the ADB!), we're a lot closer to where we're going than we were.

It may come to a surprise to my readers given the traditional very bearish sentiment expressed at this space, but I actually agree with Buttonwood and Cassandra here. However, I would simply add the important qualifier that there will be a significant asymmetry in terms of where individual economies are going as a function of where they are and were. No where is this more true in the case of Japan and as we progress to the data and analysis it should be abundantly clear that for all the talk of second derivatives and glasses being half full, Japan still look to be in an extraordinarily bad shape. Initial evidence of this comes from the headline GDP figures which don't seem to be blessed with any second derivative effects.

Final estimates from Q4 2008 suggested that Japan contracted at an annualized 12.1% which puts Japan in the dubious pole position of biggest GDP declines among industrialised economies. Q1 estimates are yet to be released, but no-one expects, I think, an improvement as the incoming data so far has been nothing but extraordinarily poor. Sociétè Generale expects Japan to contract sharply in 2009 with Q1 as an forecast bottom. I am not sure about the bottom in the sense that while it may be a bottom in the sense of the second derivative noted above, it won't likely mark a return to sustained growth.

In this note, I will provide an overview of the recent developments in the Japanese economy. Since we last convened some interesting points have emerged. For one, Japan is back in deflation measured on the US style core price index and for the first time in a very long time Japan is now running a current account deficit. This last point will be studied in some detail since it marks a very important issue for the export dependent Japanese economy both in a historical and a current perspective. Before we begin I should note that this post is very big with a lot of graphs and even an econometric model to boot. I understand full well if this deters some of my readers; I shall not hold it against you.

Prices and Consumption, where art thou?

If there is one thing which has been stable in Japan throughout this crisis it has been the persistent sluggish trend in domestic demand measured by top line household consumption expenditures as well as prices on the other hand. These two data points consequently tell an important part of the story of the lack of domestic demand in Japan or more specifically the lack of visible momentum to pull Japan out of the doldrums. One persistent feature of the initial phases of the crisis where markets and global policy makers primarily looked towards the risk of stagflation was that inflation in Japan exclusively was driven by cost-push factors in the form of headline inflation and not demand pull factors. This idea is a well established one at this point, and materialised itself in the fact that as headline inflation shot through the roof core inflation only budged slightly. It is important to point out that this inelasticity cuts both ways and as headline inflation has abated (for now), so has the spread between the two indices narrowed significantly. The underlying point here is thus two-fold. One the one hand it is dangerous to assume that inflation driven by domestic demand conditions will correlate with external headline inflation pressures which, due to global capacity constraints and global demand conditions, look set to shoot higher the minute we move even slightly beyond the current malaise. On the other hand however, we can clearly see, in Japan, that whatever trend we see for headline inflation domestically induced price pressures in Japan are virtually non-existing and now that the crisis is seriously biting Japan is set once again to retrench into deflation despite the central bank's most ardent efforts to apply measures of quantitative easing.

As I have argued before, I believe a large part of Japan's problem with deflation is demographic. In particular, I think that because Japan is basically unable to achieve growth based on domestic momentum a growth scenario strictly based on domestic activity as the one we are seeing at the moment will be de-facto deflationary. However, since Japan is largely dependent on energy imports in so far as goes its consumption of fossil fuels (i.e. a high passthrough effect) the overall inflation indice will diverge from the core of core index which, in Japan's case, is a good proxy for domestically induced price pressures. Now, I realize that my readers will be skeptical of the demographic link here, but let me at least present results that show the broken link between the general price index and core of core prices (which exclude energy and food). Thanks to a novel data set from Japan' statistical office giving us monthly inflation rates (y-o-y) for all three recorded inflation indices since 1971 we have plenty of ammunition on our hands to proceed. In the following all numbers will be based on de-trended time series which in this case simply means that I am using the first difference.

Consider then the very simple representation below which shows the correlation between the general index and core of core index over the entire sample, from 1971-1996 and from 1997-2008.

The emerging picture should be quite straightforward to interpret even for the untrained eye. Consequently, and in so far as we can consider the simple correlation coefficient a credible measure of the strenght of the connection between two variables, then this relationship has clearly deteriorated. In graphical terms we can get an impression of this by looking at the three year rolling average of the correlation between the variables.

Now, the volatility is considerable here and in fact we can see that the correlation has hit rock bottom once before , but the accumulated trend is still one of a decline in relationship between the two variables. If we want to be even more specific we can express this in the form of single linear regression where we let the general inflation index explain the core-of-core index. As is visible below, this also shows a marked decline in explanatory relationship. However, this may not be an adequate conceptualization of the issue at hand. Consequently, let us try to narrate the problem as one of headline inflation leading core-of-core inflation. This potentially brings us into the deep murky vaults of time series econometrics and I shall not belabour my readers with techniques on how to choose optimal lags here (I tried with both a quarterly and monthly). What we end up with is the following small model.

The fit is not perfect and in terms of actual prediction tool I would be weary in using this expression alone although in a standard ARMA framework one could perhaps play around with the lags of other variables. Yet, the picture is now firmly solidified as we observe a secular decline in the model's ability to model the core-of core index.

So, what the heck is this all for then? Clearly, it is difficult to show initially that demographics represent an important underlying explanatory variable in this framework. Yet, it does corresponds with the overall point expressed above that when domestic demand is unable to generate inflation exogenous energy shocks won't necessarily lead to underlying inflation dynamics. On a general note, it is thus difficult to see how Japan can avoid to enter a serious bout of deflation during the course of 2009 especially since, at this point, deflation is being pencilled in across a wide batch of economies across the globe. As will be showed below the BOJ is already coming up with ever more spectacular measures to ward off a lingering fall into deflation. There are two forward looking issues to watch out for when it comes to the comeback of deflation in Japan. One is the point that since everybody is facing deflation, and thus engaging in different forms of QE will Japan then be less of an odd man out? A second a highly related point is what will happen to the JPY in relation to the whole collective edifice of QE among OECD central banks?

Turning briefly to the consumption expenditures and thus the state of the Japanese consumer it really is (un)steady as she goes. Some analysts have expressed the opinion that the Japanese consumer has held up alright up until this point in the crisis. I am not sure what data these analysts are looking at. All I know is that the headline figure for consumption expenditures is still clocking in one negative number after the other and in this light it is difficult to see from where the much awaited boost in domestic demand is going to come from; note for example here that autosales dropped a healthy 27.9% in January. Add to this that retail sales dropped 5.8% on an annual basis with the subcomponent and you have firm evidence of a slump.

To be fair, the latest reading on consumer confidence did show an uptick in February compared to January as well as the economy watchers index which measures the performance of non tradables showed an improvement, but the accompanying comments from analysts on the ground do not provide much comfort for the outlook where most domestic companies are preparing their operations for a tough recession. Ken Worsley parses the entrails of the consumer confidence report and notes that the slight increase in the willingness to buy consumer durables is a welcome sign although the overall picture is weighed down by a mounting insecurity over job safety and thus income.

Investment, huddling up for hibernation?

If the charts for consumer spending shows us that the Japanese consumer is performing decidedly worse than past years' mean, the corresponding charts and numbers of industrial production and industrial orders resemble clear depression tendencies.

It is important to note the difference between the plots above. Consequently, what we are seeing in Japan at the moment is especially a massive slump in manufacturing and industrial production dragged down by the sharp drop in external demand. In this way, the export sector so important for Japan's growth is inexorably tied together with industrial production. In the last post the graph did not include Q4 2008 and as is readily clear from the charts above Q4 08 was the breaking point for Japan (and most others too).

This picture is confirmed if we look at the monthly reading. Since the data graphed above is from the METI, the data is lacking relatively to the present in that we only have data up until January 2009 (for the monthly chart). However, just look at that line go as if it is being pulled down by gravity itself. Needless to say that the overall index is being dragged down here even if the tertiary index, which accounts for 3 times as much as industrial production in the overall index, is holding up quite well. On an annual basis, industrial production dropped a full 31% in terms of production and 31.6% in terms of shipments. Inventories decreased on a monthly basis, but are still well above their 2000 levels which makes me wonder what kind of information the analysts claiming that Japanese companies had comparatively low inventories going into this were looking at. As for the small bounce in tertiary industry postal services seem to be the main culprit increasing with a full 11%.

As for the link between manufacturing and exports, I am going to let Danske Bank's analysts do the heavy lifting and display their wonderful graph plotting industrial production and exports.

I don't think this requires much interpretation and the main points is well articulated by Danske;

In Japan, manufacturing accounts for about 22% of GDP compared with just 17% and 12% of GDP in Euroland and the US, respectively. For that reason, there is a larger negative secondary impact on particularly investment demand from the recent collapse in global trade and industrial production.

The outlook here is thus completely dependent on where you think global growth is heading. Given the increasing indications that the slump will be prolonged the outlook is bleak. Of course, and coming back to that dreaded second derivative the decline will stabilise at some point, especially as inventories are cut. Yet, the key is the extent to which it will recover to anywhere near past levels. Surely Japan will be ready when the world is about to take off again but there is a lot to suggest that the margins on export led growth will be a lot thinner than they are now since everybody seems to be in the midst of a transition towards the same growth strategy. In this light it seems as if Japanese manufactures may indeed be tucking themselves in for a prolonged hibernation.

Evidence to suggest this came recently from the hands of Morgan Stanley analyst Takehiro Sato who had an excellent analysis looking forward to the upcoming Tankan survej of Japanese industry. The key is that companies are expected to revise down their capex and investment plans drastically. Moreover, the most recent print for industrial production in the form of the preliminary report for February indicates that industrial production in Japan contracted at an annual 38.4%. In light of this extraordinary decline, Bloomberg is running a piece with the overall point that because Japanese manufacturers have been so fast in adjusting down their inventories (getting rid of excess capacity) we will soon see a pick-up as inventories have been cleared. The logic of this argument is indisputable, but I think that the underlying point is misplaced for two principal reasons. For starters, the recovery argument only holds if in a standard cyclical downturn and since the current debacle is clearly different I am weary about applying any kind of conventional wisdom here. Obviously, if inventories go to zero we get that famous "second derivative effect" noted above, but the overall level of growth and increase in production is likely to be very low if not negative. We should Remember that there is indeed a flipside to all these horrendous numbers coming in now and this is what level we will end on and how long it will take for us to get back up.

Finally and just to show that the crisis has had a notable effect in the market too just watch the absolute horrible performance of the main Nikkei index.

I am no equity analyst so I shall not belabour this point a lot, but merely note my personal inclination to disregard Japan in terms of the global market portfolio (beta) and in stead going for some alpha through stock picking which is obviously possible even if the overall trend is inexorably down. Go for the ones with exposure outside Japan is my advice, but that should be taken with a couple of truck loads of salt and I am ready to stand corrected any time by those much smarter than me in terms of trading equities.

The External Sector, Wither Growth

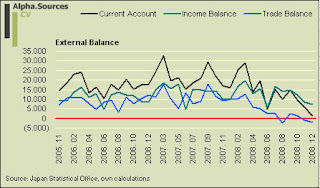

Perhaps one of the most interesting news points to come out of Japan since we last convened was the news that Japan had entered a current account deficit for the first time in a long while. This is significant for a number of reasons. First of all, it shows us the extent of the slump in that the trade balance balance has swung so fast and so much into negative territory. However, as I have argued endlessly we also need to look at income and here Japanese savers have been extraordinarily well endowed. Thus I also think that there is a technical issue to deal with here in that the income balance is likely to have swung into negative on the basis of the appreciation of the JPY we have observed in the latter part of 2008 and into the first months of 2009.

The CA deficit is not visible on the graph above but it does not take much imagination to see where the lines are going; especially not since we recently learned that Japanese exports dropped a whopping 49% year on year in February as shipments to the rest of world almost stalled completely.

Needless to say, the move of Japan's current account into deficit territory has sparked all kinds of interesting points not least in the context of Japan's impending forced rebalancing. It comes to no surprise to me that the Economist was the first to jump the gun hailing Japan's rebalancing act.

Japanese households used to be among the world’s biggest savers and, as a result, the country ran a massive trade surplus. But no longer. They now save less of their income than American households, and Japan’s trade balance moved into deficit last year (see top chart). A long-overdue—and painful—economic rebalancing is under way.

To be fair to the Economist, they do make the important qualifier that since the external balance is coming due to a collapse in external conditions rather than a shift in actual growth path it may not be exactly what the doctor ordered. Yet, the Economist also applies standard life cycle theory to suggest that as Japan grows older so will we start to observe dissaving on aggregate and thus predicts, like all those famous economic steady state models, that Japan according to theory should be running a current account deficit. I think this is way to simple and in order to move forward on this field some important adjustments need to be made to Modigliani's life cycle hypothesis and, crucially, how it applies to aggregate economies. A lot of the confusion arises in the context of Japanese households their low savings rate and the fact that Japan exactly seems to suffering from a dearth in consumption (domestic demand) and surplus of savings. In a recent piece by the New York Times this view is articulated pointing towards the obvious effect that when you have no domestic demand of any meaningful proportion you become de-facto dependent on external demand. However, Stefan Karlsson retorts that low consumer spending in Japan is the result of low growth and not the cause pointing to the historically low household savings rate in Japan.

The plot thickens and at this point we simply need to get some data on the table to see what is actually going on. As a first stab let direct the attention to three crucial issues when applying individual life cycle theory to aggregate outcomes. First, you need to distinguish between working and non-working households as the savings dynamics are bound to differ markedly. Moreover, you need to incorporate some kind of uncertainty buffer to adjust for the fact that the transversality condition does not hold and thus that consumers do not dissave to 0. Secondly, you need to look at the overall stock of savings as well as the flow to increase or decrease this stock. This is very important relative to the measure of the saving rate out of disposable income. Thirdly and intimately related to point two you need to look at the evolution of income and the change in the stock of saving relative to the change in income. With these points in mind, let us consult the data.

The first graph shows the evolution of annual income and the stock of savings and it represents an important picture since it shows us that Japanese households are indeed sitting on a large pile of savings measured as a stock even if as Scott Peterson showed us recently it is dwindling which indeed constitutes a worrying trend. The key point is of course what to do with those savings. Sure, one can spend them and dissave which is what would happen in a closed economy, but in an open economy the dynamics are likely to be strikingly different. Basically, this stock of savings represents a structural excess of savings on a stock basis and one of the only ways to make it count is to transfer it into income by investing abroad or by investing in export oriented domestic industries [1]. This is the only way that this saving can be transferred into investment and then into income. Consequently, Japan does suffer from a a chronic lack of domestic demand and consumption and it does so exactly because relying on consumption with the current demographic profile is not viable. Persons dissave, but societies do not since they don't have an end point or at least, a market economy has every interest in fighting off dissaving through the leakage of exporting excess saving. In this way, all the opinions introduced above get it wrong I feel because you really need to incorporate realistic assumptions on demographics. Take Mr. Karlsson's suggestion that Japanese households save more? Out of what I ask and assuming that these savings should be accumulated to invest later where would you invest it? At home (to what return) or abroad? This is exactly the key point since moving towards the NYT and their implicit narrative that Japan raises consumption the simple question is that she can't and understanding precisely why this is and what this means for the global economy is absolutely crucial. I shall spare no chance in pointing out this again and again.

Thus, if Japan wants growth it needs to make those savings count and oh boy have those Japs made it count.

In order to understand the graphs above you need to go back to James Hamilton's post about the paradox of thrift and in particular the simple representation of savings in an open economy. We consequently have;

Y = C + I + G + X and by definition net national savings defined as Y - C - G = I + X where X is the CA balance. [2]

Japan clearly has had, as the Economist rightly points to, a consistent surplus almost since 1980, but you need to read the fine print here. I am not saying anything about export orientation as such but more so about export dependency. In this way, let us run the following thought experiment and assume that all the talk in the 1980s about Japan unfairly sustaining a bilateral surplus towards the US represents a deliberate export oriented policy.

Now, why is this plausible? Well, look at the graph for investment as a share of GNI and witness how it actually rose towards the end of the 1980s and peaked with the bubble 1989-1991. Clearly, Japan got a strong accumulated boost from external demand throughout the 1980s which helped keep national savings high even though domestic investment rates fell. But was Japan dependent on this in terms of creating growth? This seems dubious in that investment rose sharply during the end of the 1980s and thus we can say that, all things equal, Japan had the the domestic conditions to create a sound investment boom/bust bubble.

But then we enter famous lost decade of Japan and whether be it for standard life cycle reasons or because of inept policies Japan never really managed to irk out an increase in domestic investment rates. Yet, if we add the accumulated surplus of domestic investment over domestic savings which by definition leaves the country as a leakage we get the CA surplus which despite secular declining domestic investment rates have risen. To put it more categorically, Japan has been able to save more than would have been merited by domestic capacity to absorb these savings through investment if we had a closed system.

So, and to make the final point on this. What I not saying is that this process is driven entirely and exclusively by demographics. Evidently it is not. What I am saying however is that at some along the way Japan becomes dependent on this process and thus that the mechanism by which the two is connected, that is the de-facto dependence of external demand and the existence of persistent external surpluses, need to be explored. One way to initiate this exploration is exactly to incorporate a strong demographi anchor in your macroeconomic analysis and then to realize that Japan is able to make up for the secular decline in domestic investment as predicted by life cycle theories by accumulating excess savings towards the rest of the world. In fact, given the situation with respect to consumption (C) where the base simply shrinks by the year and government spending (G) which is constrained in a number of ways the addition of growth from the CA surplus is crucial and when it dissipates as we are seeing now the edifice crumbles almost entirely.

Policy responses, stretched beyond the limit?

If you have made it this far, you will have gotten the impression that things look dire in Japan with regards economic growth, momentum as well as the outlook. However and just as the politicians in other parts of the world are digging deep in their toolboxes in order to find a remedy to the debacle, so are Japanese policy makers hard at work. Well, perhaps this is a bit exaggerated since if you are looking for extraordinary and new measures you should not be looking to Japan where both fiscal and monetary policy are following the path seen in the US, the UK, and Europe the latter in which monetary policy is lagging somewhat. So is it working?

We don't know yet, but one question which seems pressing at the moment is indeed what Japan will do as the conventional tools look fall desperately short of fixing the thoroughly broken economy.

This may be a rather hasty conclusion though. Consider for example the actions taken by the BOJ which almost makes the corresponding actions taken in the US and the UK look timid. The situation for the BOJ is a bit different than over at Kaiserstrasse, DC as well as in Treadneedle street since rates were already running very close to the zero bound when the crisis hit. In this way, one method that has been used extensively is the rapid expansion of the BOJ's balance sheet through the purchase of different categories of risky assets. This strategy seem to constitute a three pronged assault. The first attack was the announcement that the BOJ would be buyers of corporate debt (of highest A1 rating) in order to push down the lingering wide spread between the benchmark rate and the rate on A1 corporate paper. This makes sense in Japan since many companies choose to finance themselves through the FI market. Recently, Deputy Governor Hirohide Yamaguchi noted that the BOJ might have to increase its purchase of corporate to fight off what has been deemed to be extremely difficult financing conditions for Japanese companies.

Recently we got the second line of defense with the announcement that the BOJ would also be buyers of companies' subordinated debt. So far the move is only meant capitalise commercial banks where the BOJ may be pencilling in as much as a 1000 billion Yen worth of purchasing of subordinated corporate debt. On the technical side many analysts have argued that since these purchases would only boost tier two capital holding it might not address the issue at hand. Add to this that since these loans by definition could only be extended to the biggest of the commercial players small and medium sized actors would not benefit from these loans.

Finally there is the third line of defense which simply involves the BOJ moving into equities and if the debt market is a murky area then the equity market must be pitch black from the point of view of the BOJ. So far, the official purchases of equities have been suggested through different vehicles such as for example the Development Bank of Japan. Yet the time may be nearing when the BOJ has to move in to support the market in general and in this case things of course start to get decidedly messy. What kind of companies to invest in? Should the BOJ hold the market or go for "stock picking"? etc. Yet, it may seem to a prudent move all together since as Glenn Maguire, chief Asia economist at Societe Generale is quoted of saying in the FT;

“Japan’s toxic assets are essentially equities and any pick up in stock markets will be more significant for improving tier one capital,”

Given the same Hirohide Yamaguchi's recent comments that the BOJ is seriously contemplating a move back into ZIRP, it looks as if we will soon see yet another step in the central bank's fight against the crisis.

Moving on to fiscal policy it seems, and unfortunately so, that most of the recent messages from Japanese politicians are merely gloss to prepare for the upcoming elections. In this way, prime minister Aso's recent chant that Japan must ready a third stimulus package is not greeted well by observers. And then we need to add the lingering issue of Japan's already elevated, and wholly unsustainable, debt level.

Consider consequently the very valid point that the BOJ could like the Fed and the BOE move in to aggressively buy up government bonds to a higher degree than is currently the case. As such Deputy Governor Hirohide Yamaguchi has noted that increased central bank funding for the MOF might actually increase yields as investors weighed the risk concerning the public debt against the decision. Circumstantial evidence is already mounting that as the Japanese government readies one stimulus package after the other yields are reacting adversely to the interest of the MOF as issuer. Takehiro Sato pinpoints the situation well when he says;

The ultimate dilemma for the government/BoJ is that, while a half-hearted fiscal expansion may fail to overcome the downward spiral of the economy, an overblown version risks depressing market confidence in the fiscal policy.

Finally, and as Scott Peterson eloquently points out you also need to look at where the money is spent (and on what) since Japan really needs to get as much, as it were, bang for the buck.

No Way out for Japan?

I can understand if my readers and in particular those of you who have made it this far are a bit annoyed at this point. Here I go again with the doom and gloom about Japan. Well, true as this may be, let me just reiterate the main point so obviously present in the data that Japan is in an absolutely horrendous situation in economic terms. However, this does not mean that I should not be focusing on solutions. Don't worry, I am getting there, but I also want it to come out right so I am holding off my guns a bit.

Meanwhile, in this note I have attempted to hammer down some more theoretical arguments using long term data and thus a more comprehensive argument. As for the immediate economic outlook it is not particularly good. All main gauges point downwards and it is almost certain that Japan will be facing deflation in the coming quarters (if not years). This will intensify the credit crunch and further bring into doubt the sustainability of the Japanese public debt situation. This is a well known narrative, but it is important since it seriously cripples policy makers in their attempts to actually do something. On the back of this, the real sector is suffering. Most notably industrial production has stalled completely faced with the dramatic slowdown in external demand and coupled with the inability of domestic demand to take up the slack in any given sense of the word Japan is simply being pulled down by the full weight of its inability to mount a challenge towards the headwinds blowing from the global economic crisis. I call it engine failure because it is in fact what it is, a failure of the well lubricated export engine that has, when active, driven the Japanese economy in the past decade. Once again I will finish with the almost trivial point in the context of Alpha Sources' musings that this has to do with demographics and the age structure of Japanese society. The sooner all parties involved understand this, the sooner we can roll up our sleeves and get to work on solutions.

---

[1] - the observed decline in home bias among Japanese investors is an important part of the picture here.

[2] - Readers with basic mathematical inclination will notice that expressing the spread between investment and net exports and foreign asset income as the addition to national savings from external demand, is just a detour of expressing the current account balance as a share of GNI. Thus basic algebra gives;

I/GNI - I+(X-M)/GNI = [I - I + (X-M)]/GNI; (cancelling out the I's) gives (X-M)/GNI.

Italy's Economic Contraction Accelerates

by Edward Hugh: Barcelona

There is no doubt about it: Italy's economic situation has worsened considerably during the current quarter. Only last week the OECD forecast that Italy's gross domestic product is likely to fall by 4.2 percent in 2009. This follows hot on the heals of an earlier statement where the OECD said the situation in Italy this year and next was "much worse" than it had previously thought, and that Italy would not come out of its recession until "sometime" in 2010 at the earliest. According to the earlier forecast the OECD expected GDP to fall this year by one percent and then by a further 0.8 percent in 2010.

The Bank of Italy has also changed its forecast, and now suggest that GDP this year will fall by 2.6 percent. In January (the last time they revised their Italy forecast), the IMF forecast a fall of 2.1 percent. This is almost certain to be revised downwards in the April World Economic Outlook forecast review. Only today the Italian employers’ lobby Confindustria cut its forecast for 2009 GDP , saying the economy will contract by 3.5 percent while public debt will climb to 112.5 percent of GDP.

And these forecasts are not drawn like rabbits out of a hat, since evidence of the deterioration in Italy's economic performance is now to be found everywhere, but perhaps nowhere is it clearer than in the most recent exports and industrial output numbers. Italian exports plummeted 26 percent in January from a year ago, the biggest drop since records began in 1991. With the drop in exports leaving the country with a trade deficit of 3.6 billion euros.

There is no doubt about it: Italy's economic situation has worsened considerably during the current quarter. Only last week the OECD forecast that Italy's gross domestic product is likely to fall by 4.2 percent in 2009. This follows hot on the heals of an earlier statement where the OECD said the situation in Italy this year and next was "much worse" than it had previously thought, and that Italy would not come out of its recession until "sometime" in 2010 at the earliest. According to the earlier forecast the OECD expected GDP to fall this year by one percent and then by a further 0.8 percent in 2010.

The Bank of Italy has also changed its forecast, and now suggest that GDP this year will fall by 2.6 percent. In January (the last time they revised their Italy forecast), the IMF forecast a fall of 2.1 percent. This is almost certain to be revised downwards in the April World Economic Outlook forecast review. Only today the Italian employers’ lobby Confindustria cut its forecast for 2009 GDP , saying the economy will contract by 3.5 percent while public debt will climb to 112.5 percent of GDP.

And these forecasts are not drawn like rabbits out of a hat, since evidence of the deterioration in Italy's economic performance is now to be found everywhere, but perhaps nowhere is it clearer than in the most recent exports and industrial output numbers. Italian exports plummeted 26 percent in January from a year ago, the biggest drop since records began in 1991. With the drop in exports leaving the country with a trade deficit of 3.6 billion euros.

Meanwhile Italian industrial output fell for a fifth month as what is now the country's worst recession in more than 30 years forced companies to keep cutting output and jobs. Production dropped a seasonally adjusted 0.2 percent from December, when it fell a revised 3.9 percent. From a year earlier, adjusted production fell 16.7 percent, the biggest decline since records began in January 1991.

As we can see from the revised output index, after remaining pretty much stationary from early 2007, production really started to slump in May 2008, and hasn't looked back since.

Italy's manufacturing PMI fell again in February to 35.0 from January's 36.1, and was only marginally above November's series record low of 34.9.

Italian business confidence fell to a record low in March as concern that the fourth recession in seven years will damp orders more than offset lower oil prices and borrowing costs. The Isae Institute’s business confidence index dropped to 59.8, the lowest since the index was created in 1986, from a revised 63.2 in February.

Italian executives also reported having more problems getting credit in February, when the report showed that 40.2 percent of those surveyed said the credit situation worsened, up from 33.5 percent in January. The new orders sub component also fell, to minus 65 from minus 58 in January, the lowest since 1991. And manufacturers’ expectations for production over the next three months fell to minus 24 from minus 20.

Retail Sales Fall

Italian retail sales contracted for the 24th consecutive month in February as the credit crunch tightened its grip on spending, and consumers put off purchases of cars and home appliances.

Services Decline Confirms Accelerating Contraction

Italian service sector activity sank in February to its weakest level on record, the latest sign of a deepening recession in the euro zone's third largest economy, the latest Markit/ADACI PMI survey and the Index, spanning companies from hotels to insurance brokers, fell to 37.9 from 41.1 in January to hit the lowest level since the survey began in January 1998.

GDP Growth In Long Term Decline

Italian fourth quarter GDP fell a downwardly revised 1.9% from the previous quarter, the largest drop since 1980, compared with a downwardly revised 0.7% contraction in the third quarter of 2008 according to data published by the Italian statistics office Istat last week.

On a year on year basis GDP fell a downwardly revised 2.9%, also the sharpest drop since 1980.

Business investments fell by 6.9% during the quarter, consumer spending fell 0.6%, while exports plummeted 7.4%. As can be seen from the chart below, given the endemic weak state of Italian household consumption, GDP growth tends to follow export growth.

Although, of course, household consumption has now been falling back sharply since early 2007.

Although, of course, household consumption has now been falling back sharply since early 2007.

2008 data for Italian GDP has now also been published, and again the drop of 1,0% has not been seen since 1975.

Italy's economy will shrink by around 2.6 percent this year, a member of the Bank of Italy's executive board said on Wednesday, cutting the central bank's previous forecast of a 2.0 percent contraction made in January.

Since January, Italian economic data has been consistently bad, with business confidence and purchasing managers' indexes plumbing new record lows. The government pencilled in a forecast of -2.0 percent in its Stability Programme issued in February, but many analysts have cut their forecasts even lower than the BOI. Intesa San Paolo, Italy's largest bank, has a forecast of -2.9 percent.

While Italy’s unemployment rate rose in the fourth quarter to the highest in more than two years as the recession deepened, prompting companies to reduce production and jobs. Joblessness increased to a seasonally adjusted 6.9 percent from 6.7 in the previous quarter, the Rome-based national statistics office said today. The number of unemployed rose to 1.73 million in the third quarter, when 1.69 million people were out of work.

Little Room To Manouevre As The Credit Crunch Tightens

For some time now Italy’s government has been abandoning its optimistic rhetoric and adoptinmg a more sombre assessment of the economy. Giulio Tremonti, the finance minister, recently told a conference that 2009 would be “even more difficult” than last year, with two leading newspapers quoting him as saying Italy faced a “horrible year”.

Tremonti said the government would look next week at providing more to help the growing numbers of unemployed, on top of €8bn it says has already been set aside for extra benefits.

Italian consumer confidence fell for the first time in three months in March, with the Isae Institute’s consumer confidence index dropping to 99.8 from a revised 104 in February.

Growing evidence suggests that the crisis is really hitting the Italian economy in a kind of back-to-front fashion, with the slump in the real economy (and especially the economic crisis in the East of Europe) threatening to drive Italian banks into more and more difficulty. The finance minister is under growing pressure from other cabinet members to increase government spending further, but understandably, Tremonti keeps pointing to Italy’s huge public debt as a major impediment to any serious stimulus plan. So it is simply a question of grin and bear it.

Tremonti admitted at a recent meeting with banks, companies and unions that Italy had seen a greater credit market conditions tightening in recent months than most other eurozone economies. On the other hand he pointed to the fact that Italian banks had shown a “strong interest” in taking up the government-backed bond offer (which only totals €12bn) at the same time as he rejected criticism that the 8.5 per cent interest rate they carry was too high.

Intesa Sanpaolo, which is Italy’s biggest bank by market value, has announced that it will apply for 4 billion euros worth of the bonds after it posted a 1.23 billion-euro fourth-quarter loss on writedowns. This makes Intesa the third Italian lender to take advantage of the country’s bank aid package, following similar decisions by Banco Popolare and UniCredit.

At the same time the credit crunch is evidently producing some sort of housing crisis and the sale of residential properties dropped 15 percent last year, according to OMISE, a government agency that specializes in collecting data on real estate. Property specialists Nomisma forecast house prices will fall 8.5 percent in the second half of 2009, and for a country which has not seen much of a housing boom, this drop is significant. Italian Prime Minister Silvio Berlusconi has announced a housing plan designed to make it easier for property owners to carry out home modernisation. According to Il Sole, Italians will be able to add as much as 20 percent of the current size of their homes without planning formalities. This is obviously rather controversial, and Bank of Italy Governor Mario Draghi was himself pretty non commital in his testimony before a parliamentary commission last week, resticting himself to saying that the “plan could act as a stimulus, although the short-term effect on economic growth is uncertain.”

Moody's Cuts Slovakia's Outlook

by Edward Hugh: Barcelona

Now here's an interesting story. Slovakia has just joined the eurozone, a status most of the rest of the EU's East European members would badly like to attain. But just to remind us that joining the zone, while offering considerable support and protection in times of trouble, is no panacea, Moody's Investors Service have last Friday cut their outlook on Slovakia’s government bonds rating (to stable from positive, implying their is no likelihood of an upgrade in the near future, a possibility which was implicit in the earlier positive outlook).

Moody's justify their decision on the grounds that future investment in Slovakia is at risk due to a combination of factors: the recession in the euro-region, the country’s dependence on the car industry and its falling competitiveness compared with other eastern European nations, many of whose currencies have fallen sharply during the crisis. In fact the Slovak Finance Ministry forecast only last Friday that foreign direct investment into Slovakia will be much lower this year than originally expected - with the Minister stating he expected a decline in FDI to 0.6 percent of gross domestic product in 2009, compared with a 2.7 percent forecast before the economic and financial crisis hit the country.

The worrying thing for me about all this, is not the immediate short term pressure which Slovakia will undoubtedly be under due to the regional crisis, but rather the loss of competitiveness issue, becuase it is ringing bells in my head about what previously happened in the case of Portugal (see my lengthy post on this here). The danger is that eurozone membership gets to be seen as a target you strive to achieve, and then relax into once it has been attained. The Southern Europe experience generally is not encouraging in this regard, and as they are finding out now, the hardest work begins after adopting the euro, since there is no currency left to devalue should loss of competitiveness prove severe.

So I really do wish Jean Claude Trichet would exercise some of that famous "vigilance" on what to do about this issue too, since the long term future of the currency zone undoubtedly depends on getting this one right.

In fact investors are already positioning themselves for a future weakening in the country's creditworthiness. Slovak five-year credit default swaps have been falling back recently, after hitting an all time high of 133.1 earlier in the month, according to CMA Datavision prices. (A basis point on a credit-default swap contract protecting 10 million euros of debt from default for five years is equivalent to 1,000 euros a year).

But the spread on Slovak government bonds has also been rising (see chart below), and the spread with the 10 year government bond vis a vis the German equivalent was 136.7 on Friday. The chart presents a pretty preoccupying picture, since while bond spreads have all been under pressure since the onset of last October's crisis, it is unusual to see investors perceiving credit risk rising in a country which has only just joined the "gold-digger" club. And Friday's warning shot from Moody's needs to be understood in this context.

The country has seen a huge increase in its car manufacturing capacity in recent years, fueling double-digit economic growth in the quarters before the financial crisis, but amid waning western European demand for Slovak-made cars - including brands Volkswagen, Audi and Peugeot - the country now faces a stalling economy and rising unemployment. Slovak unemployment data for February showed the jobless rate reaching its highest level in more than two years, rising to 9.7% from 9% in January.

Over 75% of the country's EUR332 million stimulus has now been spent, largely giving tax breaks to low-wage earners to encourage them to reenter the work force, and with a fiscal deficit ceiling of 3% of GDP to defend, spending cuts rather than stimulus cannot be ruled out, since VAT returns are falling fast.

So while Slovakia's total public debt only equals around 30% of GDP, pressure on the spread could increase if the country is forced to increase its borrowing. Slovakia only expects to need EUR 5 billion in borrowing this year, and EUR 2.5 billion has already been secured in the first few months of the year.

Strong Economic Slowdown Underway

The Slovak economy slowed further in the fourth quarter of last year with real GDP growing by 2.5 percent year on year. Whole year GDP for 2008 was 6.4 percent with total GDP reaching €67.33 billion. Economic growth had been 6.6 percent in the third quarter, and while there is no official data for seasonally adjusted quarter on quarter growth, I estimate the economy may well have contracted by around 1.5%.

Part of the problem is the drop in export demand for Slovakia's car driven economy, and the country posted a trade deficit in January, as drop in demand was made worse by the suspension of gas deliveries from Russia. Exports slumped 29.9 percent on the year in January, the fourth consecutive monthly decline, and the biggest drop at least since 2006 when the statistics office began compiling data under the current methodology. Imports were down 22.4 percent.

The trade deficit totalled 279.5 million euros ($361 million), following a revised deficit of 341.6 million euros in December. Slovakia posted a trade surplus of 42.3 million euros in January 2008.

The drop in the demand for exports has obviously hit industrial production which decreased by 27 % year-on-year in January reach the biggest drop since the statistics office began compiling data in 1999. Manufacturing output fell 32,7 %.

Construction output was also down sharply in January, falling by 25.6% year on year, although seasonal factors can obviously be playing a part here.

Slovak retail sales fell by 3.3% year on year and totalled €1.3bn in January 2009. The largest contributing factor to this overall decrease was from the category of ‘other household goods in specialised shops’ retail which dropped by 24%. In addition sales of fuels ‘in specialised shops’ retail (15.6%) and the category of ‘retail sales realised not in stores’ (4.8%) experienced significant drops. Retail sales of electronics fell sharply (42.5%), and drops were also witnessed in the categories of: ‘food in specialised shops’ (15.8%); recreation and entertainment (12.7%); other goods in specialised shops retail (5.9%); and retail in non-specialised shops (4.5%).

Worry Now, So As Not To Pay The Price Later

In the short term the Moody's decsion really doesn't mean that much, since Slovakia only had 28.6% (of GDP) in gross debt in 2008, but it is the mid and longer term dynamic we need to think about. Slovakia is about to issue a 2-year zero-coupon bond for an unspecified amount today, but the government debt agency is unlikely to have problems. However, as we have already seen in the cases of Ireland, Greece, Portugal and Spain, simply becoming a member of the eurozone is not a guarantee of anything in economic performance terms (although it does provide almost automatic protection from short term balance of payments crises). So it is important that Slovakia takes the appropriate measures to restore competitiveness now, otherwise we could see the horrifying spectacle of the eurozone's newest member steadily moving over to stand alongside countries like Greece, hovering around near the exit door, struggling desperately to avoid being rocketed out.

Now here's an interesting story. Slovakia has just joined the eurozone, a status most of the rest of the EU's East European members would badly like to attain. But just to remind us that joining the zone, while offering considerable support and protection in times of trouble, is no panacea, Moody's Investors Service have last Friday cut their outlook on Slovakia’s government bonds rating (to stable from positive, implying their is no likelihood of an upgrade in the near future, a possibility which was implicit in the earlier positive outlook).

Moody's justify their decision on the grounds that future investment in Slovakia is at risk due to a combination of factors: the recession in the euro-region, the country’s dependence on the car industry and its falling competitiveness compared with other eastern European nations, many of whose currencies have fallen sharply during the crisis. In fact the Slovak Finance Ministry forecast only last Friday that foreign direct investment into Slovakia will be much lower this year than originally expected - with the Minister stating he expected a decline in FDI to 0.6 percent of gross domestic product in 2009, compared with a 2.7 percent forecast before the economic and financial crisis hit the country.

The worrying thing for me about all this, is not the immediate short term pressure which Slovakia will undoubtedly be under due to the regional crisis, but rather the loss of competitiveness issue, becuase it is ringing bells in my head about what previously happened in the case of Portugal (see my lengthy post on this here). The danger is that eurozone membership gets to be seen as a target you strive to achieve, and then relax into once it has been attained. The Southern Europe experience generally is not encouraging in this regard, and as they are finding out now, the hardest work begins after adopting the euro, since there is no currency left to devalue should loss of competitiveness prove severe.

So I really do wish Jean Claude Trichet would exercise some of that famous "vigilance" on what to do about this issue too, since the long term future of the currency zone undoubtedly depends on getting this one right.

In fact investors are already positioning themselves for a future weakening in the country's creditworthiness. Slovak five-year credit default swaps have been falling back recently, after hitting an all time high of 133.1 earlier in the month, according to CMA Datavision prices. (A basis point on a credit-default swap contract protecting 10 million euros of debt from default for five years is equivalent to 1,000 euros a year).

But the spread on Slovak government bonds has also been rising (see chart below), and the spread with the 10 year government bond vis a vis the German equivalent was 136.7 on Friday. The chart presents a pretty preoccupying picture, since while bond spreads have all been under pressure since the onset of last October's crisis, it is unusual to see investors perceiving credit risk rising in a country which has only just joined the "gold-digger" club. And Friday's warning shot from Moody's needs to be understood in this context.

The country has seen a huge increase in its car manufacturing capacity in recent years, fueling double-digit economic growth in the quarters before the financial crisis, but amid waning western European demand for Slovak-made cars - including brands Volkswagen, Audi and Peugeot - the country now faces a stalling economy and rising unemployment. Slovak unemployment data for February showed the jobless rate reaching its highest level in more than two years, rising to 9.7% from 9% in January.

Over 75% of the country's EUR332 million stimulus has now been spent, largely giving tax breaks to low-wage earners to encourage them to reenter the work force, and with a fiscal deficit ceiling of 3% of GDP to defend, spending cuts rather than stimulus cannot be ruled out, since VAT returns are falling fast.

So while Slovakia's total public debt only equals around 30% of GDP, pressure on the spread could increase if the country is forced to increase its borrowing. Slovakia only expects to need EUR 5 billion in borrowing this year, and EUR 2.5 billion has already been secured in the first few months of the year.

Strong Economic Slowdown Underway

The Slovak economy slowed further in the fourth quarter of last year with real GDP growing by 2.5 percent year on year. Whole year GDP for 2008 was 6.4 percent with total GDP reaching €67.33 billion. Economic growth had been 6.6 percent in the third quarter, and while there is no official data for seasonally adjusted quarter on quarter growth, I estimate the economy may well have contracted by around 1.5%.

Part of the problem is the drop in export demand for Slovakia's car driven economy, and the country posted a trade deficit in January, as drop in demand was made worse by the suspension of gas deliveries from Russia. Exports slumped 29.9 percent on the year in January, the fourth consecutive monthly decline, and the biggest drop at least since 2006 when the statistics office began compiling data under the current methodology. Imports were down 22.4 percent.

The trade deficit totalled 279.5 million euros ($361 million), following a revised deficit of 341.6 million euros in December. Slovakia posted a trade surplus of 42.3 million euros in January 2008.

The drop in the demand for exports has obviously hit industrial production which decreased by 27 % year-on-year in January reach the biggest drop since the statistics office began compiling data in 1999. Manufacturing output fell 32,7 %.

Construction output was also down sharply in January, falling by 25.6% year on year, although seasonal factors can obviously be playing a part here.

Slovak retail sales fell by 3.3% year on year and totalled €1.3bn in January 2009. The largest contributing factor to this overall decrease was from the category of ‘other household goods in specialised shops’ retail which dropped by 24%. In addition sales of fuels ‘in specialised shops’ retail (15.6%) and the category of ‘retail sales realised not in stores’ (4.8%) experienced significant drops. Retail sales of electronics fell sharply (42.5%), and drops were also witnessed in the categories of: ‘food in specialised shops’ (15.8%); recreation and entertainment (12.7%); other goods in specialised shops retail (5.9%); and retail in non-specialised shops (4.5%).

Worry Now, So As Not To Pay The Price Later

In the short term the Moody's decsion really doesn't mean that much, since Slovakia only had 28.6% (of GDP) in gross debt in 2008, but it is the mid and longer term dynamic we need to think about. Slovakia is about to issue a 2-year zero-coupon bond for an unspecified amount today, but the government debt agency is unlikely to have problems. However, as we have already seen in the cases of Ireland, Greece, Portugal and Spain, simply becoming a member of the eurozone is not a guarantee of anything in economic performance terms (although it does provide almost automatic protection from short term balance of payments crises). So it is important that Slovakia takes the appropriate measures to restore competitiveness now, otherwise we could see the horrifying spectacle of the eurozone's newest member steadily moving over to stand alongside countries like Greece, hovering around near the exit door, struggling desperately to avoid being rocketed out.

Friday, March 27, 2009

Two Graphs That Tell It All On Spain

by Edward Hugh : Barcelona

First, the one year Euribor reference rate, which has been falling since the ECB started lowering interest rates in the autumn of last year.

And secondly the chart showing the average rate of interest charged by Spanish banks on new mortgages, which as we can see, has been rising steadily since December 2007.

The average interest rate charged by Spanish banks for new mortgages in January 2009 was 5.64%, meaning that the average cost of a new mortgage had gone up by 10.2% over January 2008 (when the rate was 5.1%), and by 1.1% when compared with December 2008. Meanwhile the Euribor reference rate looks set to close this month at all time record lows of 1.91%. In January - the last month for which we have data on mortgage lending - the Euribor rate was 2.27%.

The reasons lying behind this upward movement in Spanish mortgages are twofold. On the one hand the Spanish banks are having increasing difficulty raising finance due to their perceived risk level, and on the other they themselves have have been forced to raise the risk premium they charge to clients due to the rising levels of non performing mortgages they have on their books.

Basically what this means is that the ECB policy isn't working in Spain, and that despite the massive quantities of liquidity provided, the monetary conditions continue to tighten, and doubly so give that the real value of the rates charged (ie the inflation adjusted value) keeps rising automatically as inflation falls.

Mortgage lending in Spain more than halved in January while the number of homes started in the fourth quarter dropped an annualy 62 percent. The 51.7 percent year on year fall in mortgage lending for urban dwellings was the steepest in 12 straight months of decline.

House sales fell in January by 38.6 percent, figures published earlier this month showed, and Housing Ministry data showed the foundations of only 40,737 homes were laid in the fourth quarter - 62 percent fewer than in the fourth quarter of 2007, and 27 percent down on the preceding quarter. During 2008 as a whole, Spanish builders started 360,044 homes - a 41.5 percent fall on 2008. On the other hand 633,228 homes were completed last year, reflecting the optimist which prevailed in 2006/07 when the buildings were started at the height of the boom in 2006-07.

Spain has a supply overhang estimated at almost any number you like over 1 million unsold homes (the minimum estimate, and no one really knows), or more than three times the number of new households created each year in Spain.

The number of mortgages offered has crashed as banks restrict credit given forecasts non-performing loans will reach around 9 percent next year, while unemployment is now likely to rise above 4.5 million by years end, up from the current 3.5 million.

As I indicated in this post yesterday, we are moving from a situation where people the banks were afraid to lend, to one where people become increasingly afraid to borrow (since they don’t know when they will lose their jobs, or even their homes), with Spain's citizens becoming more and more reluctant to take on additional debt due to fears they could be caught in the next round of job losses.

As a result January mortgage lending falling to 6.47 billion euros, while the rate of new bank lending to households dropped to 3.9% year on year.

Spanish debt defaults leapt 197 percent in 2008, with construction and property firms accounting for 4 of every 10 failures. The number of firms and individuals that filed for administration rose to 2,902, the highest level on record, according to Spain's National Statistics Institute. Also bad loans at Spanish banks rose by 15.3 percent in January, the sharpest monthly increase since property developer Martinsa Fadesa filed for administration in July. Bad loans rose more than 9 billion euros to 68.18 billion in January compared with an average monthly rise in the last six months of around 5 billion euros.

The non-performing loans (NPL) ratio for all institutions was at 3.8 percent in January, up from 3.3 percent in December, with rates among savings banks the highest at 4.45 percent compared with 3.79 percent a month earlier. Commercial banks had an NPL ratio of 3.17 percent, up from 2.81 percent. In fact Spain's financial institutions have seen NPLs more than quadruple in the last 12 months from 16.23 billion euros in January 2008.

Spain's savings banks, responsible for about half the country's loans and the most exposed to the property market downturn, could see NPLs rise to 9 percent by 2010, according to the saving banks association.

What To Do With The Bad Banks?

As a result of all this a furious public row (unusual in Spain) has broken out over what to do with the broken banks.

The Spanish Economy Minister Pedro Solbes has said the government is prepared to recapitalise healthy banks but suggested that those with serious solvency problems should seek a merger rather than look for state aid.

What he has in mind is that the troubled banks should turn to Spain's privately-funded Deposit Guarantee Fund (FGD) should they need capital injections to make tie-ups viable. However, the insurance fund holds only 7.2 billion euros in bank contributions, and since this is orders of magnitude less than the size of the problem it is obvious the government will end up having to putting money into the recapitalisation process, and especially into the Savings Bank sector, since the Spanish press has been reporting that 20 of Spain's 45 savings banks are now considering mergers. And it is obviously only a matter of time before one of the mid-sized Spanish banks like Popular, Sabadell or Banesto joins the consolidation process.

Clearly many of those most directly involved in the banking industry are laothe to accept the Solbes formula, since wuite simply they cannot afford it. And this was made pretty clear by Francisco Gonzalez, chairman of Spain's second largest bank BBVA, when he pointed out last week that nationalisation of the bad banks was the only realistic way forward.

Two Spanish regional savings banks have already reached a preliminary merger deal - Unicaja, based in Spain's southern Andalucia region, and the smaller Caja Castilla La Mancha (CCM), located in the central-southern province of the same name - following talks which were carefully brokered by the Bank of Spain. Clearly this merger willl need to be followed by a capital injection from Spain's Deposit Guarantee Fund to help them clean up the "troubled assets" which will naturally be found in the combined accounts of the new bank which emerges. Many other such regional caja "weddings" are obviously soon to follow. But the big question is, where will all the financing come from? It is pretty clear that the problem which is building up is bigger than Spain can handle alone, and finance (not loans) from the European Union will be needed, with centrally backed EU Bonds being the most likely mechanism with which to fund the injection.

First, the one year Euribor reference rate, which has been falling since the ECB started lowering interest rates in the autumn of last year.

And secondly the chart showing the average rate of interest charged by Spanish banks on new mortgages, which as we can see, has been rising steadily since December 2007.

The average interest rate charged by Spanish banks for new mortgages in January 2009 was 5.64%, meaning that the average cost of a new mortgage had gone up by 10.2% over January 2008 (when the rate was 5.1%), and by 1.1% when compared with December 2008. Meanwhile the Euribor reference rate looks set to close this month at all time record lows of 1.91%. In January - the last month for which we have data on mortgage lending - the Euribor rate was 2.27%.

The reasons lying behind this upward movement in Spanish mortgages are twofold. On the one hand the Spanish banks are having increasing difficulty raising finance due to their perceived risk level, and on the other they themselves have have been forced to raise the risk premium they charge to clients due to the rising levels of non performing mortgages they have on their books.

Basically what this means is that the ECB policy isn't working in Spain, and that despite the massive quantities of liquidity provided, the monetary conditions continue to tighten, and doubly so give that the real value of the rates charged (ie the inflation adjusted value) keeps rising automatically as inflation falls.

Mortgage lending in Spain more than halved in January while the number of homes started in the fourth quarter dropped an annualy 62 percent. The 51.7 percent year on year fall in mortgage lending for urban dwellings was the steepest in 12 straight months of decline.

House sales fell in January by 38.6 percent, figures published earlier this month showed, and Housing Ministry data showed the foundations of only 40,737 homes were laid in the fourth quarter - 62 percent fewer than in the fourth quarter of 2007, and 27 percent down on the preceding quarter. During 2008 as a whole, Spanish builders started 360,044 homes - a 41.5 percent fall on 2008. On the other hand 633,228 homes were completed last year, reflecting the optimist which prevailed in 2006/07 when the buildings were started at the height of the boom in 2006-07.

Spain has a supply overhang estimated at almost any number you like over 1 million unsold homes (the minimum estimate, and no one really knows), or more than three times the number of new households created each year in Spain.

The number of mortgages offered has crashed as banks restrict credit given forecasts non-performing loans will reach around 9 percent next year, while unemployment is now likely to rise above 4.5 million by years end, up from the current 3.5 million.

As I indicated in this post yesterday, we are moving from a situation where people the banks were afraid to lend, to one where people become increasingly afraid to borrow (since they don’t know when they will lose their jobs, or even their homes), with Spain's citizens becoming more and more reluctant to take on additional debt due to fears they could be caught in the next round of job losses.

As a result January mortgage lending falling to 6.47 billion euros, while the rate of new bank lending to households dropped to 3.9% year on year.

Spanish debt defaults leapt 197 percent in 2008, with construction and property firms accounting for 4 of every 10 failures. The number of firms and individuals that filed for administration rose to 2,902, the highest level on record, according to Spain's National Statistics Institute. Also bad loans at Spanish banks rose by 15.3 percent in January, the sharpest monthly increase since property developer Martinsa Fadesa filed for administration in July. Bad loans rose more than 9 billion euros to 68.18 billion in January compared with an average monthly rise in the last six months of around 5 billion euros.

The non-performing loans (NPL) ratio for all institutions was at 3.8 percent in January, up from 3.3 percent in December, with rates among savings banks the highest at 4.45 percent compared with 3.79 percent a month earlier. Commercial banks had an NPL ratio of 3.17 percent, up from 2.81 percent. In fact Spain's financial institutions have seen NPLs more than quadruple in the last 12 months from 16.23 billion euros in January 2008.

Spain's savings banks, responsible for about half the country's loans and the most exposed to the property market downturn, could see NPLs rise to 9 percent by 2010, according to the saving banks association.

What To Do With The Bad Banks?

As a result of all this a furious public row (unusual in Spain) has broken out over what to do with the broken banks.

The Spanish Economy Minister Pedro Solbes has said the government is prepared to recapitalise healthy banks but suggested that those with serious solvency problems should seek a merger rather than look for state aid.

"In cases where banks have acted correctly in relation to solvency and the health of their accounts...logically they could receive support," Solbes said in a speech to an economic conference in Madrid. "Banks that are unable to remain solvent and clean up their accounts should cease to be players in the financial system so they don't generate distortions in the public sector."

What he has in mind is that the troubled banks should turn to Spain's privately-funded Deposit Guarantee Fund (FGD) should they need capital injections to make tie-ups viable. However, the insurance fund holds only 7.2 billion euros in bank contributions, and since this is orders of magnitude less than the size of the problem it is obvious the government will end up having to putting money into the recapitalisation process, and especially into the Savings Bank sector, since the Spanish press has been reporting that 20 of Spain's 45 savings banks are now considering mergers. And it is obviously only a matter of time before one of the mid-sized Spanish banks like Popular, Sabadell or Banesto joins the consolidation process.

Clearly many of those most directly involved in the banking industry are laothe to accept the Solbes formula, since wuite simply they cannot afford it. And this was made pretty clear by Francisco Gonzalez, chairman of Spain's second largest bank BBVA, when he pointed out last week that nationalisation of the bad banks was the only realistic way forward.

"When a bank shows signs of extreme weakness the authorities should take control of it, which implies removing the directors and reducing or eliminating share capital in the institution," Gonzalez said at a conference in Madrid.Governments should then appoint a new team to separate toxic assets from healthy ones and quarantine them in publicly controlled funds, the chairman said, advocating a level of state intervention not yet seen in Spain. "Then the bank would be privatised again through a transparent sale to private companies," he said, without making specific reference to Spanish banks.